The North-South divide is back at the top of the political agenda. Andy Burnham's proposal for a "Number 10 North," an outpost of the Prime Minister's office based in Manchester, has put regional inequality back into daily headlines, reopening a familiar national debate: does the UK still work better for some places than others?

But for organisations in credit, utilities and collections, the more useful question isn't where political power sits. It's where financial pressure sits. Regional inequality is not only an economic or political issue, it may also have implications for how affordability pressures emerge across customer populations. The central distinction is clear: the largest debt balances may sit in the South, but the strongest indicators of financial distress such as debt advice demand, insolvency and affordability pressure suggest that financial vulnerability is more felt in the North.

This raises an interesting question for creditors. While customer treatment should always be driven by individual circumstances, do regional patterns in financial resilience offer an additional lens through which organisations can better understand emerging affordability pressures and customer outcomes?

Why this is in the news? Following Keir Starmer's announcement that he will stand down as Labour leader, Andy Burnham, the frontrunner to succeed him, has proposed relocating part of the Prime Minister's office to Manchester, arguing that economic decision-making is too London-centric. The proposal has revived debate about regional inequality across housing, income and public investment.

This piece takes no position on the merits of the proposal. It uses the renewed attention on regional inequality as a starting point for looking at what the data says about financial resilience across the UK.

Income Still Draws the Line

Discussions around the North-South divide often focus on income and economic growth, but the underlying differences in financial resilience remain equally significant.

ONS data shows that gross disposable household income per head stood at £35,361 in London in 2023, compared with £19,977 in the North East, against a UK average of £24,836.

Disposable income remains one of the strongest indicators of financial resilience, customers with less in their pocket after their essential spends are less able to manage rising bills, absorb financial shocks or maintain repayment commitments when circumstances change.

Higher-income households are often able to support larger borrowing commitments because they have greater income and asset buffers. By contrast, customers with relatively modest balances can experience significant financial stress if essential costs consume a greater proportion of their income.

This distinction is becoming more important as household budgets come under sustained pressure across the UK.

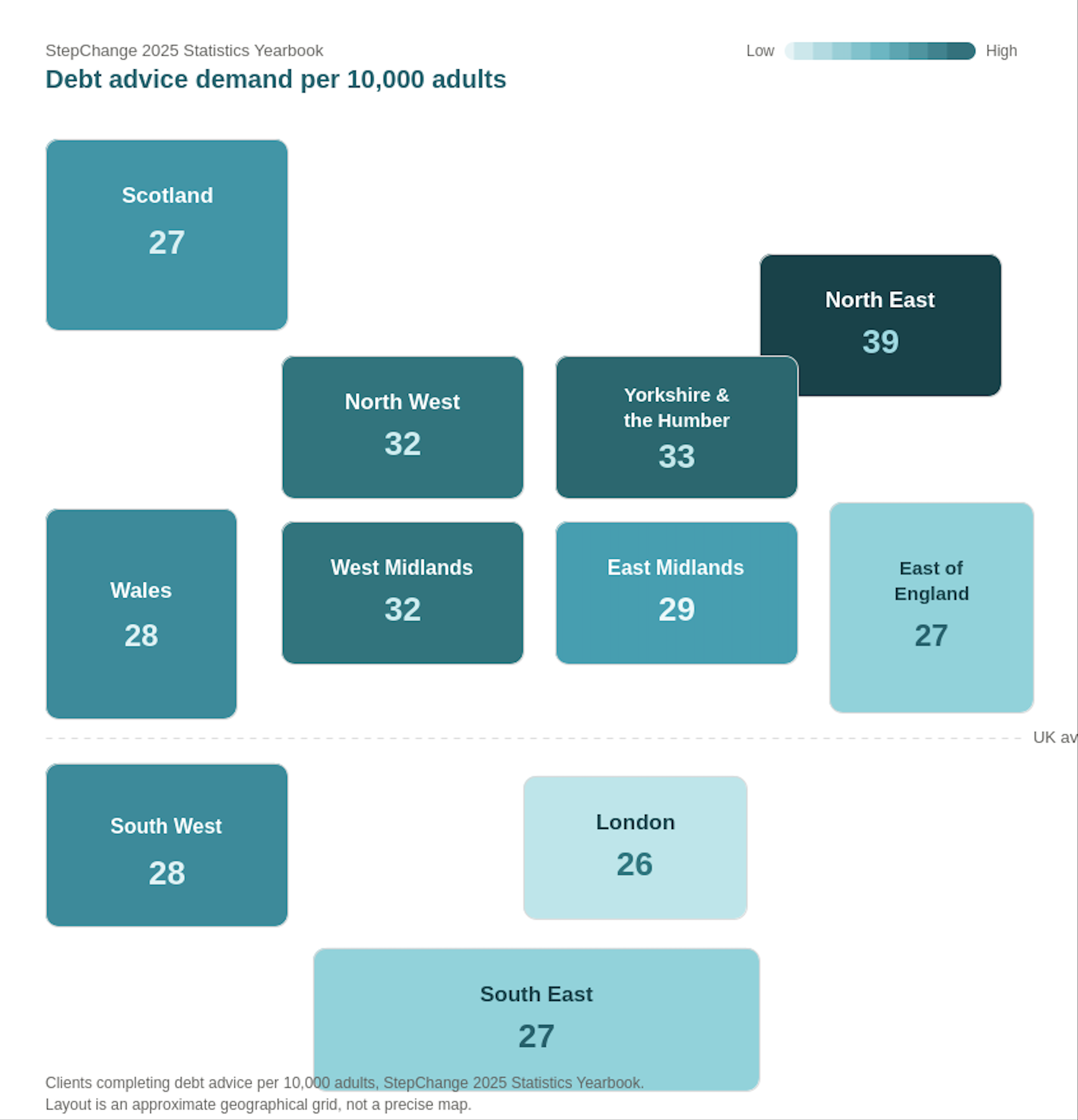

Where the Pressure Really Lives

StepChange's 2025 Statistics Yearbook recorded 163,916 new clients completing debt advice and reported significant regional variation in demand. The North East recorded 39 clients per 10,000 adults, compared with a UK average of 28 and just 26 per 10,000 adults in London. Yorkshire and the Humber reported 33 per 10,000 adults, while both the North West and West Midlands recorded 32.

The same pattern whereby areas associated with lower disposable income generate proportionately higher demand for debt advice appears within insolvency data. The Insolvency Service reported that the individual insolvency rate in England and Wales was 25.3 per 10,000 adults in 2025. The North East recorded the highest rate at 33.8, while London recorded the lowest at 16.2. Areas including Halton, Kingston upon Hull and Blackpool reported some of the highest insolvency rates nationally.

This raises a question as to whether indicators of financial distress are emerging differently across various parts of the country. For companies seeking to better understand affordability trends within their customer base, regional patterns could provide useful context alongside the individual customer-level insights that remain central to decision-making.

The Bills That Show It First

Some of the strongest evidence of affordability pressure is increasingly found in essential household bills.

StepChange reported that average household arrears among its clients increased from £3,911 in 2024 to £4,345 in 2025. It also reported that 37% of clients were in energy arrears, 33% were in council tax arrears and 22% were in water arrears, with average energy arrears reaching £2,560 and average council tax arrears exceeding £2,100.

National utility data tells a similar story. Ofgem reported that, in Q1 2026, 1.13 million electricity customers and 908,840 gas customers were in arrears without a repayment arrangement. Average arrears among those customers reached £1,876 for electricity and £1,623 for gas.

These measures show where affordability pressure is already translating into financial difficulty. Energy, water and council tax arrears rarely exist in isolation, often signalling wider pressure across a household's financial commitments.

As essential costs continue to rise, it is worth considering whether affordability challenges may emerge differently across regions with varying levels of income, household resilience and exposure to cost pressures. Understanding those trends does not replace assessing individual circumstances, but it could help organisations better understand the environments in which their customers are operating.

The Next Bill Everyone Will Feel

The water sector's ‘Big Upgrade’ infrastructure programme brings this into sharper focus.

Significant investment is required across the sector and customers will ultimately experience much of that investment through bills. However, while the requirement for investment is national, customers' ability to absorb those costs may vary considerably.

Support mechanisms such as social tariffs and affordability schemes vary between providers, meaning customers in similar financial circumstances may receive different support depending on where they live.

This creates an interesting affordability question. If national cost increases are experienced by households with very different levels of financial resilience, what impact might this have on financial outcomes across different regions?

The issue extends beyond water and applies equally to customers facing increasing pressure from essential costs whilst food and fuel continue to rise. Whilst treatment decisions should always be based on the specific circumstances of the individual customer, understanding how affordability pressures are developing more broadly may become increasingly relevant.

The Question Creditors Can't Ignore

The evidence highlights that affordability pressures and indicators of financial distress do not always appear evenly distributed across the UK.

The FCA's expectations around vulnerability, affordability and Consumer Duty rightly focus on the individual circumstances of the person in front of us. A customer experiencing financial difficulty in Newcastle should receive the same fair and appropriate consideration as a customer experiencing financial difficulty in Southampton.

The more relevant question may be whether broader regional trends can provide additional insight into how affordability pressures are evolving within customer populations.

As affordability pressures continue, organisations may wish to consider whether they have sufficient visibility of:

- regional concentrations of arrears and customer vulnerability;

- areas with higher debt advice demand and insolvency activity;

- geographic differences in repayment sustainability;

- the impact of regional utility and council tax costs on customer affordability;

- whether current segmentation models reflect changing affordability pressures within certain communities.

The challenge is not to identify customers based on where they live. Rather, it could be to understand whether wider economic and affordability trends can help organisations better anticipate where financial pressure may emerge and ensure support is available when customers need it.

What the data does suggest to us, is that financial resilience, affordability pressures and indicators of distress may not always be distributed evenly across the country. As economic conditions continue to evolve, companies may increasingly find themselves asking whether regional patterns provide an early signal of emerging affordability risk.

For organisations seeking to deliver good customer outcomes, that may be an area worth exploring.

Whatever shape devolution ultimately takes, the data suggests financial resilience is already unevenly distributed across the UK. That is a present-day operational reality for creditors, regardless of how the political debate unfolds.

How Arum can help

Understanding changing affordability dynamics is becoming increasingly important for creditors, utilities and servicing organisations.

At Arum, we work with lenders, debt purchasers, utilities and collections organisations to understand evolving customer affordability challenges and assess whether existing strategies remain effective in a changing environment.

This includes:

- reviewing collections and servicing strategies against affordability and vulnerability indicators;

- assessing segmentation models and treatment pathways;

- identifying emerging concentrations of customer risk;

- strengthening affordability and vulnerability frameworks;

- supporting Consumer Duty and customer outcome assessments;

- helping organisations balance sustainable recoveries with fair customer outcomes.

As affordability pressures continue to evolve, organisations that combine account-level insight with a broader understanding of the economic environment in which their customers operate will be better positioned to deliver both effective collections performance and positive customer outcomes.

Get in touch: chloe.charles@arum-global.com / christie.maitland@arum-global.com

Ultimately, the debate may not be whether a North-South divide exists in debt. The more interesting question is whether geographic patterns can help organisations better understand how affordability pressures are changing across the customers they serve.

About The authors

Chloe Charles

Chloe is a Senior Consultant at Arum Global, specialising in collections strategy, systems, and operational improvement. With a strong academic foundation from Warwick Business School, Chloe works closely with clients across financial services and utilities to deliver practical, data-led solutions that improve customer outcomes and performance. She brings a thoughtful, client-first approach to navigating regulatory change and advancing modern collections practices.

Christie Maitland

Christie is a senior Analyst at Arum Global, specialising in systems and data-led solutions. Christie has strong experience within utilities and banking working with a number of our international clients. Christie brings an analytical and strategic viewpoint to the data, bringing it to life for our clients.